See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To expect the unexpected shows a thoroughly modern intellect.” – Oscar Wilde

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view yesterday’s CNBC segment discussing yesterday’s sell-off and Nasdaq 5% pullbacks, in general, click on the image below.

After trading lower overnight, equity futures are higher across the board this morning following comments from New York Fed President John Williams, who says the Fed has room to lower rates in the short-term as weakness in the labor market poses a bigger risk than inflation. In response, S&P 500 futures are up 0.5% while Nasdaq futures are up slightly less. For both indices, the rebound is nowhere near enough to make up for yesterday’s declines, let alone getting us anywhere near the intraday highs from less than 24 hours ago.

Crude oil and 10-year yields are both lower, gold is basically flat, and crypto is seeing steep losses with Bitcoin and Ether both down about 4% while less ‘blue-chip’ coins in the space are down even more.

After yesterday’s weakness, it should come as no surprise that Asian stocks were creamed overnight, putting them all deep in the red for the week. European stocks are also lower, but not by the same degree, as the STOXX 600 is down 0.8%, but all major indices on the continent are on pace for weekly losses of at least 2%.

What started out yesterday as a Dr. Jekyll moment yesterday quickly turned into a Mr. Hyde event as the S&P 500, led by tech, turned a gain of nearly 2% into a decline of over 1.5%. Bulls started off the day strutting their stuff, got a little nervous as they headed out to lunch, and then came back ready to throw up.

Within the S&P 500, there were some major reversals. 13 stocks in the index closed more than 10% lower than their intraday high, which is nearly unheard of for large-cap stocks unless there’s a stock-specific event causing the move. Looking at the list of the biggest intraday reversals, not only were eight of them from the Technology sector, but most of the ones that aren’t were still AI-adjacent stocks.

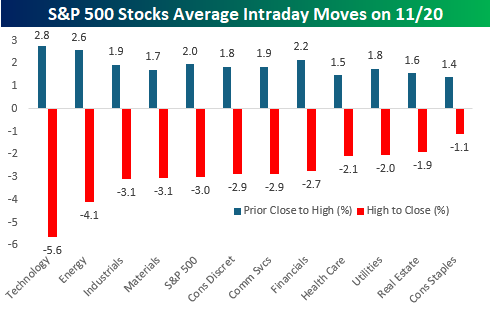

While tech led the reversal, it wasn’t solely about Tech. Within the S&P 500, 420 stocks traded down from the open to close, and the average stock in the S&P 500 finished the day down more than 3% from its intraday high. The chart below shows the average change of individual stocks yesterday from Wednesday’s close through the intraday high and then the intraday high to the close.

Tech stocks rallied the most initially, with an average gain of 2.8% and then reversed an average of 5.6% from the open to close. Besides Technology, though, the only two sectors where the average decline from the intraday high to the close was less than 2% were Consumer Staples (-1.1%) and Real Estate (-1.9%). In three sectors besides Technology (Energy, Industrials, and Materials), the average decline was more than 3%. So, again, Tech led the way but it had plenty of company.