See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There’s no such thing as simple. Simple is hard.” – Martin Scorsese

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s looking (for now) like another positive start to the week as S&P 500 and Nasdaq futures are indicated higher. We say for now, because the tone was much more positive before the sun came up on the East Coast. In fact, futures on the Dow have actually moved into negative territory while the Nasdaq’s gain has been whittled down to 0.25%. The primary driver of the Nasdaq’s gain is a 4% rally in Alphabet (GOOGL) following news that Berkshire Hathaway acquired 18 million shares during Q3.

After moving up as high as 4.15% on Friday, the 10-year yield is down over 3 bps to 4.11%, crude oil is flat and barely hanging on to $60 per barrel, gold is modestly lower, and Bitcoin is higher, reversing overnight weakness that took its YTD performance negative for the year.

The week started on a mixed note in Asia. South Korean stocks rallied close to 2% as Samsung and SK Hynix rallied, but Japan and China both traded lower on geopolitical concerns after China advised citizens not to travel to Japan following comments made by the new Japanese PM Takaichi, regarding Taiwan. JGB yields in Japan also moved higher as the 20-year yield hit its highest levels since 1999.

European stocks started off the week higher but have reversed lower since the open and are now down across the board as the STOXX 600 falls 0.5%, led lower by a 1% drop in Spanish stocks.

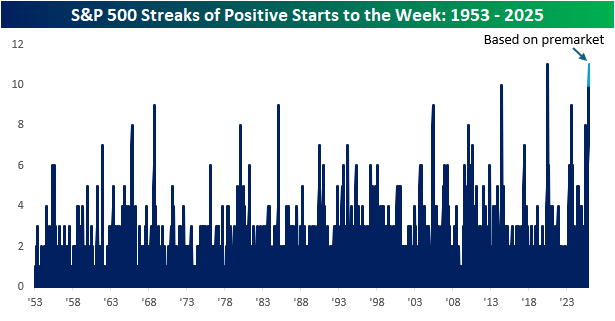

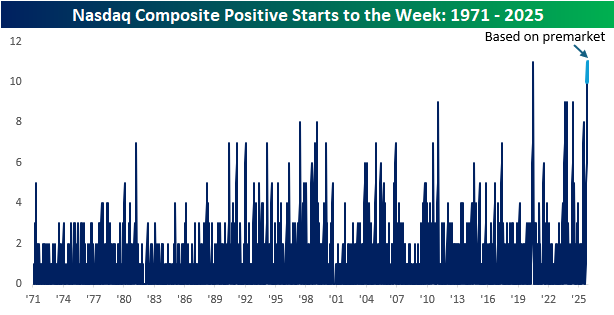

Futures don’t look as positive as they did earlier, but as of this writing, they’re still higher, and if that pace remains the case, it will be historic for both the S&P 500 and Nasdaq. Heading into this week, both indices have had positive returns on the first trading day of the week for ten straight weeks, which was one short of each index’s respective record streak from July 2020 coming out of the Covid crash lows.

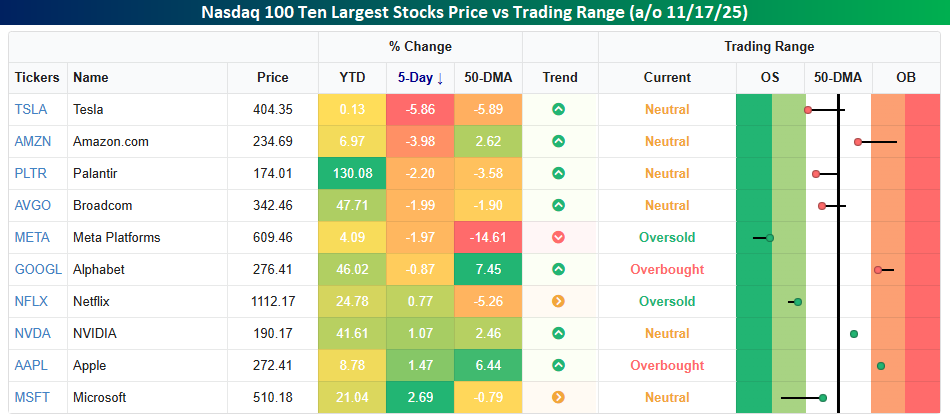

Within the Nasdaq, there’s been some bifurcation in returns lately. On a YTD basis, the ten largest stocks in the index are all still up, but the range of returns varies widely. Palantir (PLTR) easily leads the group with a gain of over 130%, but three others in the top ten are still up at least 40% YTD. Last week, though, returns were much more scattered. Led lower by Tesla’s (TSLA) decline of nearly 6%, five of the ten largest stocks in the index were basically down at least 2%. At the other end of the spectrum, Microsoft (MSFT), Apple (AAPL), and Nvidia (NVDA) were all up over 1%.

Relative to their respective 50-DMAs, the ten largest stocks are also all over the place. Meta (META) is an extreme as it closed out the week nearly 15% below its 50-DMA, but TSLA and Netflix (NFLX) are also more than 5% below their 50-DMAs as well. Meanwhile, two stocks in the S&P 500 – Alphabet (GGOGL) and AAAPL) – are more than 5% above their 50-DMAs.