See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“And so we always say we’re not on a preset path, and we really mean that.” – Jerome Powell

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are lower this morning with the S&P 500 and Nasdaq both indicated to open moderately lower from yesterday’s close as investors continue to digest Powell’s hawkish comments from yesterday. The weakness also follows a slew of earnings reports, including the behemoths of Alphabet (GOOGL), Meta (META), and Microsoft (MSFT). The reaction from the market to those three has been somewhat of a draw, with GOOGL up sharply, META down sharply, and MSFT only modestly lower. The fun continues tonight with just as many reports, including Amazon.com (AMZN) and Apple (AAPL) after the bell. After that, we’ll be through the peak of earnings season, at least in terms of market cap, so Congress better get the government open again, so there can be some economic data to focus on!

In Asia, there was no shortage of headlines with Presidents Trump and Xi meeting in South Korea. While the two leaders reached a 1-year détente on trade with Trump reducing fentanyl tariffs to 10%, China agreed to keep the flow of rare earth materials going and announced plans to purchase soybeans, energy, and other farm products. President Trump also said he plans to visit China in April. Despite all the headlines, though, it was a quiet session as most indices in the region were modestly lower. Of course, South Korea bucked the trend, though, with a gain of 0.1% as the KOSPI remains seemingly unstoppable.

In European trading this morning, stocks are decidedly lower. The STOXX 600 is down 0.5% as Spain leads the way lower with a decline of just over 1%, while Germany outperforms, even as it faces a decline of 0.1%. GDP growth for the region was above expectations (0.2% vs 0.1%), as growth in France led the region. The underperformance from Spain, however, stems from a higher-than-expected inflation print as y/y CPI increased 3.1% versus expectations for an increase of 2.9%.

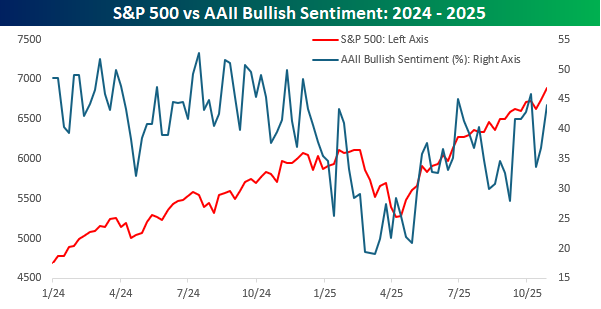

As US equities continue to march to new record highs, individual investor sentiment got a boost this week as the weekly survey from AAII showed that bullish sentiment increased from 36.9% to 44.0% for the highest reading in three weeks. While you would expect bullish sentiment to rise, current levels of optimism are nowhere near where they were at this point last year.

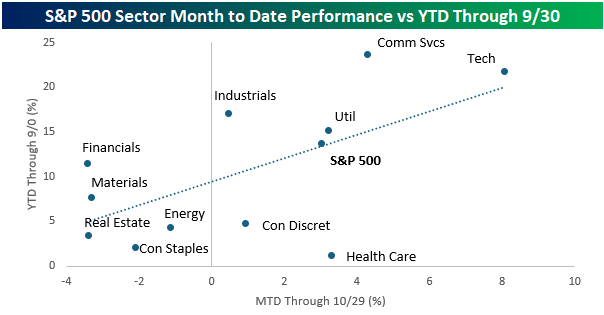

Perhaps one reason investors are less optimistic is due to the government shutdown, which has lasted nearly a month. With the S&P 500 up over 3% this month, it doesn’t appear as though the market is all that concerned, but looking at sector performance, there have been some shifts this month. The chart below compares sector performance so far in October (period covering the shutdown) on the x-axis to sector performance in the first nine months of the year (y-axis).

While sectors like Technology, Utilities, Energy, Real Estate, Materials, and Consumer Staples have stayed relatively close to the trendline, indicating that their YTD trend has remained largely intact this month, sectors like Communication Services, Health Care, Consumer Discretionary, Industrials, and Financials have seen their performance trend this month deviate significantly from their YTD trend in the first nine months of the year. That doesn’t necessarily mean that the shutdown has had a direct impact on these sectors’ performance, but their YTD trends have shifted.