See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We are like chameleons, we take our hue and the color of our moral character, from those who are around us.” – John Locke

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a positive start to the week, stocks are taking a breather this morning as S&P 500 and Nasdaq futures are indicated just fractionally higher, while a 5%+ rally in UnitedHealth (UNH) in reaction to earnings has the Dow indicated to open up closer to 0.40%. The muted gains in the US follow what has mostly been a modestly negative session in Asia and Europe.

The pace of earnings has really picked up, and tomorrow will be the biggest day of earnings season in terms of market cap with Microsoft (MSFT), Alphabet (GOOGL), and Meta (META) all on deck to report. Besides earnings reports, this morning we’ll also get the October Richmond Fed report and Consumer Confidence at 10 AM Eastern.

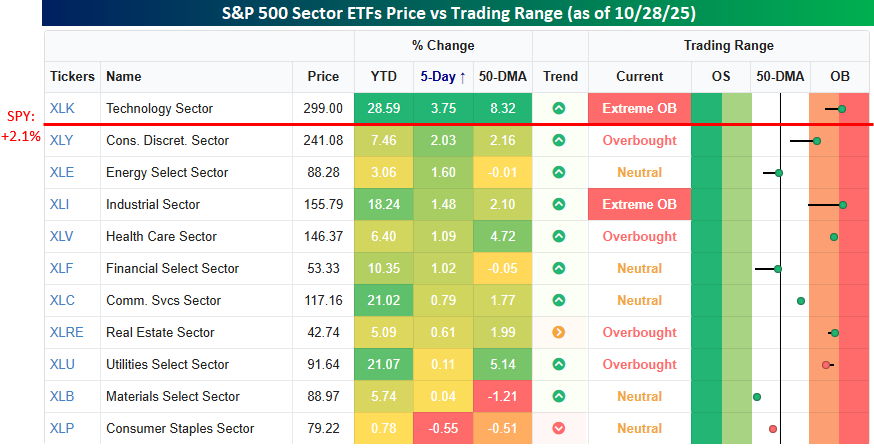

It’s been quite a week for stocks as the major US equity indices have broken out to new record highs, and S&P 500 7000 has entered the conversation. As noted in yesterday’s Chart of the Day, though, breadth has been somewhat weak. Another example of that weak breadth is in overall sector performance. As shown in the snapshot below showing sector ETF performance, over the five trading days ended yesterday, the only one outperforming SPY is Technology (XLK) with a gain of 3.75%. Consumer Discretionary (XLY) is close (2.03% vs 2.10%) but not good enough. Besides XLY, the only two other sector ETFs whose performance is within even one percentage point of the S&P 500 are Energy (XLE) and Industrials (XLI).

At the other end of the spectrum, the sectors underperforming are mostly what you would expect to see in an environment where the market rallies. Consumer Staples (XLP) is the lone decliner with a loss of 0.55% while Materials (XLB) and Utilities (XLU) have only seen modest gains of 0.10% or less. While XLU has underperformed over the last week, it remains one of just three sectors with a gain of more than 20% on the year.

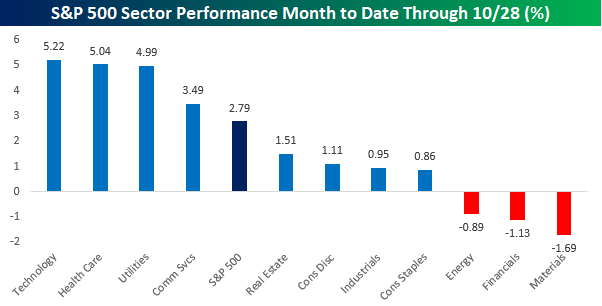

Shifting focus, with the government shutdown now set to enter its fifth week at midnight tonight, we wanted to look at how sectors have performed so far this month to see what, if any, impact it has had on performance. With a gain of 2.8% MTD through yesterday, it’s hard to say that the market has been impacted. Leading the way higher, Technology, Health Care, and Utilities have all seen gains of 5% or more, while Communication Services is the only other sector that has outperformed the S&P 500. To the downside, Materials (-1.69%), Financials (-1.13%), and Energy (-0.89%) are the only sectors to have experienced declines. It’s also worth noting that Consumer Discretionary has managed a gain of just over 1%, so even with so many Americans relying on the Federal government for either pay or benefits, and those paychecks and benefits poised to dry up, at least temporarily, it appears that the sector has held up.

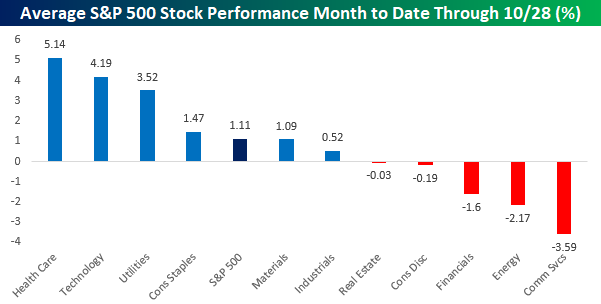

There’s always a but, though. If we look at sector performance on an unweighted basis, performance for the month looks much different. For the market as a whole, while the cap-weighted index is up 2.79%, on an unweighted basis, the gain is less than half that at 1.11%. One of the most notable shifts in performance, though, is in the Consumer Discretionary sector where the 1.11% gain on a market cap weighted basis shifts to a decline of 0.19% on an unweighted basis as MTD gains in the sector’s trillion dollar stocks (Amazon.com and Tesla) don’t carry nearly the weight on an equal-weighted as they do on a cap weighted basis.