See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“‘That didn’t work’ is cool, but ‘that won’t work’ is not a way to go through life.” – John Mayer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

A triple play from Taiwan Semiconductor (TSM)—beating on earnings, revenue, and guidance—is lifting US equity futures, with technology stocks at the forefront. This rally is notably happening despite the President stating yesterday after the close that, “We are in one now,” in reference to a trade war with China. There are also signs that China’s aggressive stance on rare earth exports could be backfiring, as it has started to cause a more unified front between the US and other international partners.

Today was supposed to be a busy one for economic data, but the government shutdown put the kibosh on that, and the only report released was the Philly Fed Manufacturing report, which came in weaker than expected. The pace of earnings, however, remains active, and once again this morning, we’re seeing generally strong results.

Outside of equities, crude oil is fractionally higher but still well below $59 per barrel, the 10-year yield is trying to hang on to 4%, gold and other precious metals are rallying (what else is new), and crypto is also rallying after what has been a rough week for the sector.

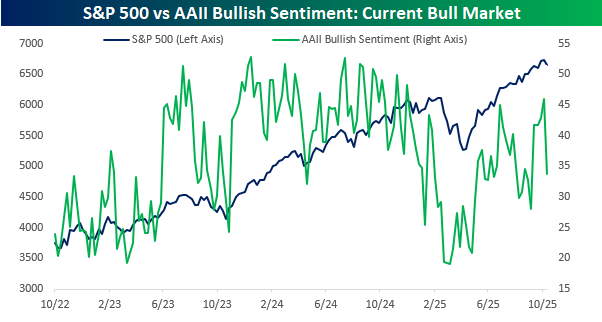

It’s been a somewhat rocky week for US equities, although by the standards of October, it’s hard to get too worked up. After trading at an all-time high intraday last Thursday, the S&P 500 closed modestly lower on the day. That modest decline was followed on Friday by a sharp 2.7% decline in the S&P 500 as trade issues with China and concerns over corporate credit in the auto sector nudged investors to take some risk off the table. This week started on a positive note as the S&P 500 erased half of the losses from last Thursday and Friday, but intraday trading has been more volatile, and there’s been more of a tendency to sell rips than buy dips.

The skittishness showed up in investor sentiment this week as the weekly American Association of Individual Investors (AAII) survey showed that bullish sentiment dropped from 45.9% to 33.7% for the lowest reading in a month. The decline in bullish sentiment comes even as the S&P 500 closed within 2% of a record high yesterday. While bullish sentiment was routinely near 50% throughout 2024 as the market rallied, in the bounce off the April lows, investors have been much less willing to hop on the bandwagon.

Along with the modest weakness in US stocks over the past five trading sessions, global equities have also been under pressure. Of the US-traded ETFs tracking the stock markets of the seven G7 countries, all but France (EWQ) traded lower in the five trading days ended yesterday, and the US was stuck right in the middle with a decline of 1.2%. The biggest laggards have been Italy (EWI) and Germany (EWG) as their the only two below their 50-DMAs. Markets have certainly been on a tear this year as six of the seven ETFs listed have rallied at least 20% this year, but in the short run, they’ve mostly worked off their overbought conditions as France is the only country still in extended territory.