See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Pessimism never won any battle.” – Dwight Eisenhower

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If the market rallies on a bank holiday, does it count? Judging by the declines in US equity futures and cryptocurrency markets, it appears not. S&P 500 and Nasdaq futures point to a drop of about 1% at the open, which would erase about two-thirds of Monday’s gain. Declines in the crypto space look even scarier as Bitcoin drops 4% and Ethereum traded back down below $4,000 with a decline of nearly 7%.

The catalyst for this morning’s weakness stems from continued trade tensions with China as both countries start charging additional fees on each other’s cargo ships, and China imposed further sanctions on certain US shipping subsidiaries. The weakness also comes even after a strong batch of earnings reports on what is really the first busy day of earnings for the Q3 reporting period.

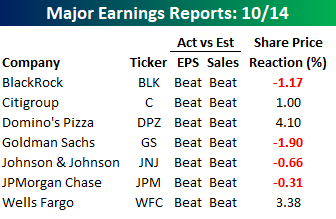

As shown in the table below, of the seven major reports this morning, all seven reported better-than-expected EPS and sales, but only three are trading higher in reaction to the reports. Domino’s (DPZ), Wells Fargo (WFC), and Citigroup (C) are all up 1% or more, while Goldman (GS) leads the declines with a drop of nearly 2%.

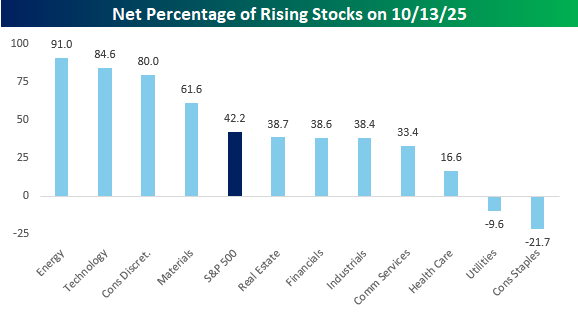

The S&P 500 had a good day to start the week yesterday, but breadth wasn’t exactly strong, especially for a day when the index rallied over 1.5%. As shown in the chart below, only four sectors saw a net of 50% or more of their components finish higher on the day. Energy and Technology led the charge with 90%+ of each sector’s components finishing higher on the day, while Consumer Discretionary (+80%) and Materials (+62%) were the only two other sectors where net breadth was stronger than the S&P 500. On the other end of the spectrum, Consumer Staples (-22%) and Utilities (-10%) both had negative net breadth, while Health Care also was relatively weak at just 17% net positive.

What was unique about yesterday’s trading, though, was that it was an extreme ‘inside’ day for the S&P 500 tracking ETF (SPY). An inside day in the market occurs when the intraday high for a day stalls out short of the prior session’s high, while the intraday low is higher. Not only did we have an inside day yesterday, but the intraday high was 1.3% below Friday’s high, while the intraday low was 1.1% above Friday’s low. We finished the day stuck right in the middle of the prior day’s range!

Inside days in SPY where both the intraday high and intraday low were more than 1% below or above the prior session’s extreme have been extremely rare. Since 1993, there have only been 11 other occurrences, with the most recent occurring back in April, right after the tariff-tantrum low. But before that, you have to go back to December 2020, and then before that, August 2015.