See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life starts all over again when it gets crisp in the fall.”- F. Scott Fitzgerald

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 was only down 0.55% yesterday, but that was enough to be the worst day for US stocks since the first trading day of the month. This morning, futures are showing modestly positive gains, with the S&P 500 up 0.13% and the Nasdaq trading 0.21% higher. Treasury yields are also higher as the 10-year has ticked up to 4.13% and is on pace for the fifth daily increase in the six trading days since last week’s cut. Crude oil is up 1% and back up to $64 per barrel for the first time since the middle of the month, but gold is giving back some of the gains from the last two days as it trades back down to $3,800 per ounce. It’s been a rough few days for crypto, but the sector is catching a break this morning as Bitcoin rallies more than 1% while Ethereum is up a more modest 0.55%.

Overnight in Asia, stocks were mixed, with Japan and China trading higher, while India and South Korea slid by about 0.5%. As we saw in many European PMI readings yesterday, Japan’s flash Manufacturing PMI slid further into contraction, falling from 49.7 to 48.4 versus forecasts for a more modest drop to 49.5.

European markets are more negative this morning, with the STOXX 600 trading down 0.3%, as luxury stocks drag the major averages, especially in France, lower.

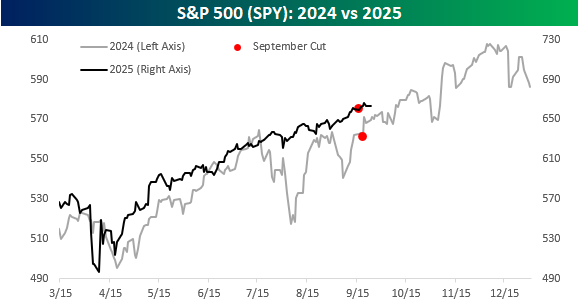

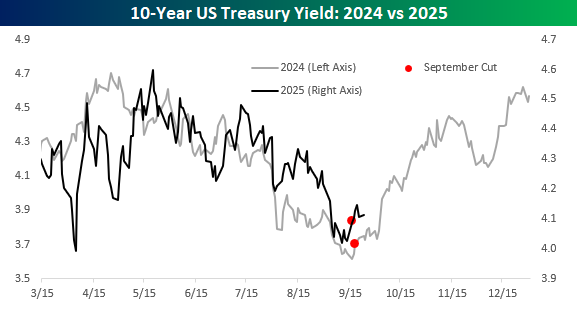

It’s been a week now since the Fed cut rates, and so far the equity market has seen a modestly positive reaction while treasury yields have moved higher, with the 10-year yield moving up to 4.11% from 4.03% last Tuesday, the day before the cut. The rise in yields over the last week undoubtedly is at least partially a reflexive response to what happened after last year’s cut. Back then, yields were in a steady decline in the six months leading up to the cut, falling from 4.7% to just over 3.6%, but the cut rang the bell, and from there, rates retraced all their previous decline by year’s end.

This year, we’ve seen a similar pattern where yields steadily declined leading up to last week’s cut and have been moving higher ever since. The one difference is that last year, most investors expected yields to continue falling into year-end, while this year, the consensus is expecting yields to rise and the curve to steepen. Will history repeat itself, or is it too obvious?

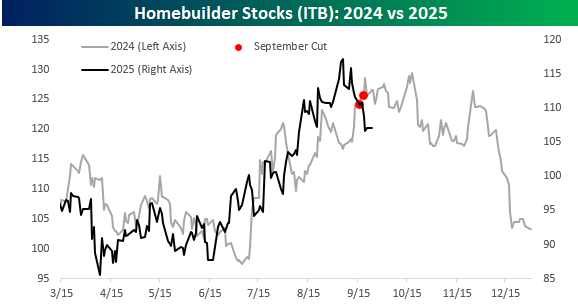

Homebuilder stocks are one of the most interest rate-sensitive sectors of the market, and like treasury yields, they’ve followed a similar pattern this year compared to last year. The one difference is that while the iShares Homebuilder ETF (ITB) was hitting highs for the year at the time of last year’s September cut, this year the ETF peaked about two weeks before last week’s cut. The fact that investors were starting to take profits in the homebuilders ahead of the cut illustrates the sentiment that there was less optimism towards long-term yields continuing lower after the September cut this year, compared to last year.

The S&P 500’s pattern this year varied from last year in that it has been much less volatile leading up to the cut than it was last year. In each case, though, it was trading either right at or very close to new highs at the time of the cut.