See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Time lost can never be recovered.” – Erik Larson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

In terms of economic activity, last week’s ISM Services report was better than expected and firmly in growth territory at 52.0, but the ISM Manufacturing and August payrolls reports both missed expectations, lending some credence to the idea that the economy is showing signs of slowing. This week, the focus will shift to inflation with Wednesday’s PPI and Thursday’s CPI reports for August. Secondary indicators of inflation have shown some upward pressure, so the market is clearly more concerned with these indicators coming in hot. How hot is the question? While a September cut next week is likely a done deal, the pace of cuts moving forward from there will hinge in large part on how ‘bad’ the inflation data is. Come Thursday morning, the market will either be only thinking about stagflation or three cuts between now and year-end.

It’s been a slow start to the week stateside, and the only economic report on the calendar this morning is the NY Fed’s Survey of Consumer Expectations, and the focus of that will be inflation expectations. Futures are modestly higher, along with crude oil, gold, and crypto.

Asian equities started off the week positive. The Nikkei rallied 1.5% closing just shy of a new high, while China was up a little less than 0.5%. Japanese GDP for Q2 came in better than expected, and China’s trade surplus handily beat expectations.

In Europe, equities kicked off the week on a positive note. The STOXX 600 is up about 0.3% as Spain and Germany lead the way higher. Investor sentiment from Sentix came in weaker than expected and declined modestly from August, but Industrial Production in Germany managed to exceed forecasts with a slightly better than expected increase.

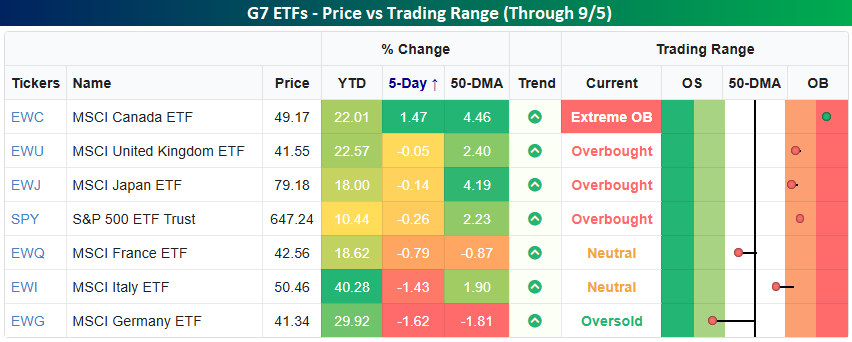

Last week was literally a middle-of-the-road week for the S&P 500. As shown in the snapshot of the ETFs tracking the equity markets of each of the G7 countries, the SPDR S&P 500 ETF’s decline of 0.26% from the close on 8/28 (due to last Monday’s Labor Day holiday) was right in the middle relative to the other six country ETFs. Canada (EWC) was the big winner of the group with a gain of 1.47% while every other ETF traded lower. Performance in the UK (EWU) and Japan (EWJ) was less bad than the US, while Germany (EWG) and Italy (EWI) both declined over 1%, and France (EWQ) fell 0.79%.

With respect to their trading ranges, Germany is the only country in the G7 trading at oversold levels, while France is the only other one trading below its 50-DMA. At the other end of the spectrum, the US and the three other countries that outperformed it last week are all at overbought or ‘extreme’ overbought levels (2+ standard deviations above their 50-DMAs).

While the US was right in the middle of the road last week, with its 10.44% YTD gain, it is still easily the weakest performer among the G7. In fact, the next closest performer is Japan with a gain of 18% while Italy is up over 40%!