See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Happiness is good health and a bad memory.” – Ingrid Bergman

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s all over. With Labor Day falling as early on the calendar as it possibly can, today marks the unofficial last trading day of Summer. Not surprisingly, futures are glum. The S&P 500 is indicated to open 0.3% lower, while Nasdaq futures are down by a more substantial 0.5%. The 10-year yield is trading modestly higher (less than 2bps), and the 4.22% yield is near the lowest level since April. Crude oil is fractionally lower, while natural gas is modestly higher. Gold is seeing modest losses, but cryptocurrencies are down by larger amounts, with Bitcoin down 2% and trading under $110K while Ethereum is down closer to 3% and trading below $4,350.

It may be the last summer Friday of the year, but the economic calendar is packed with data. Starting at 8:30, we’ll get Personal Income and Spending along with PCE and Wholesale Inventories. At 9:45, we’ll get the August Chicago PMI, which is expected to come in at 46.5, and that would be a modest downtick from July’s reading of 47.1. Finally, consumer sentiment from UMich will hit the tape at 10 AM. After a weaker-than-expected preliminary reading on 8/15, the headline reading is expected to remain unchanged at 58.6.

In Asia, the Nikkei was fractionally lower but finished the week higher. Japanese economic data was weak, with both Retail Sales and Industrial Production coming in significantly weaker than expected. While the weakness in those reports was disappointing, Tokyo CPI also came in lower than expected, which was positive. In China, shares of Alibaba (BABA) are higher following reports that the company is rolling out AI chips designed to fill the void left by the ban on Nvidia (NVDA) exports to the country.

Like the picture for US futures, European equities are also firmly lower as the STOXX 600 is trading down 0.5% taking its week-to-date decline to 2%. Country-specific equity benchmarks are also down across the board by similar amounts, although Spain is seeing outsized losses with a decline of over 1%. Banks are notably weak in the region following UK proposals to tax banks to pay down deficits.

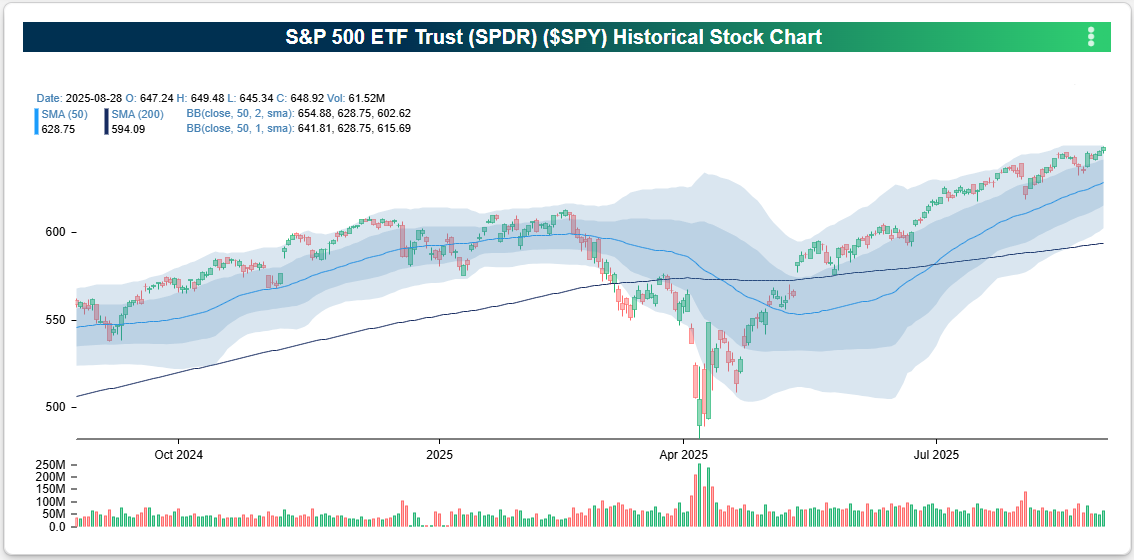

Heading into this last trading day of the summer, the S&P 500 has been in rally mode, notching its 20th record closing high of the year, rallying over 2% since last Thursday, and trading well into short-term overbought territory.

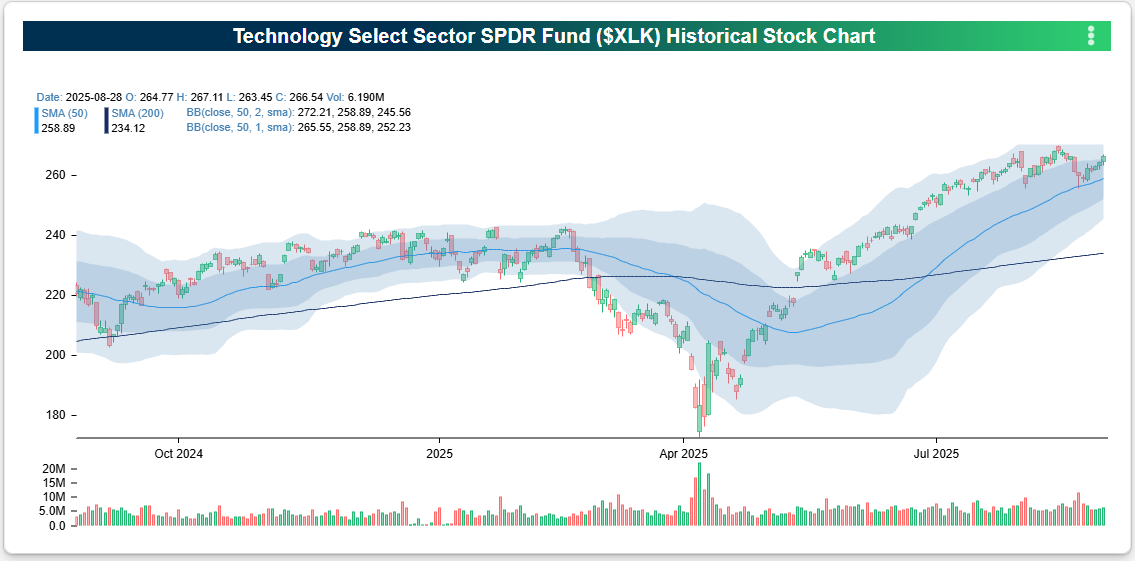

One interesting aspect of the rally is that the new highs have come without the Technology sector making new highs in tow. The sector hasn’t exactly been lagging, but it hasn’t made a new high since August 13th.

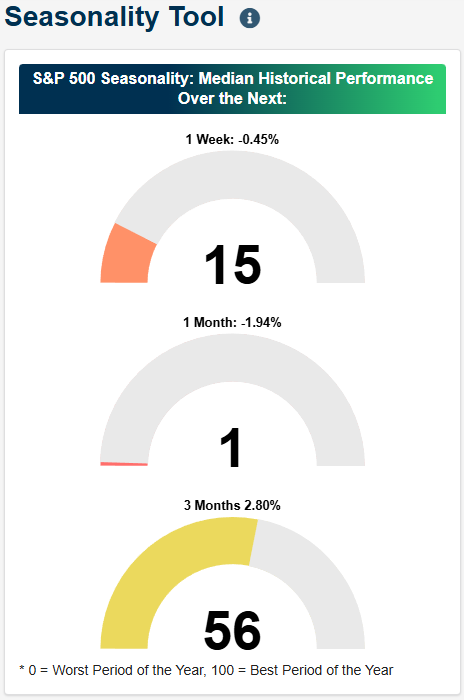

If the rally is to continue in the short term, the market will also need to do it without seasonality working in its favor. As shown in the Seasonality tool on our website, the S&P 500’s median performance over the next week based on the last ten years of data has been a decline of 0.45% which ranks in the 15th percentile of all one-week readings throughout the year. The median one-month performance has been a decline of 1.94% which is among the worst one-month periods of the year! As bad as that is, the median three-month performance is positive at 2.8% which ranks in the 56th percentile of all rolling three-month periods. Historically, the last three months of the year have been positive, but we still have to get through September first!