See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Solving big problems is easier than solving little problems.” – Sergey Brin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are set for another lower open this morning, just as the Fed kicks off its annual Jackson Hole symposium and tomorrow’s speech by Fed Chair Powell. Shares of Walmart (WMT) are down close to 4% after the company reported weaker-than-expected EPS. If the stock closes down today, it would mark the third consecutive negative reaction to earnings, the longest such streak since 2021. Outside of WMT, the earnings calendar is relatively quiet this morning, but it’s a busy day for economic data, with jobless claims (higher than expected) and the Philly Fed (weaker than expected) at 8:30, PMIs at 9:45, and then Leading Indicators and Existing Home Sales at 10:00 AM.

The weakness in US futures follows what has been a weak morning in Europe, where the STOXX 600 is down 0.3% while Asian stocks were mixed, with Japan falling 0.7% and China, India, and South Korea all finishing the session with modest gains.

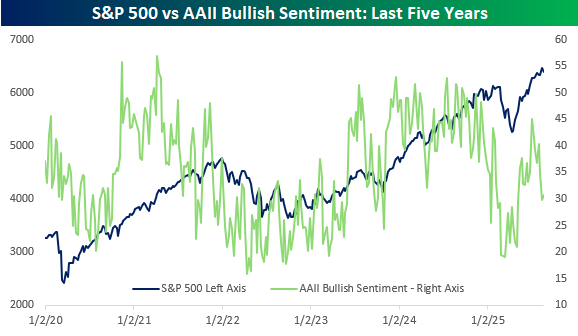

A four-day losing streak for the S&P 500 hasn’t done much to improve what has already been subdued sentiment on the part of individual investors. In this week’s survey from AAII, bullish sentiment rose slightly to 30.8% from 29.9% but with the S&P 500 within 2% of 52-week highs, investors aren’t happy. As shown in the chart below, a similar divergence emerged between equities and bullish sentiment earlier in the year, right before the market started to unravel. Then again, from early in 2021 and throughout the year, sentiment steadily deteriorated while the market just marched higher.

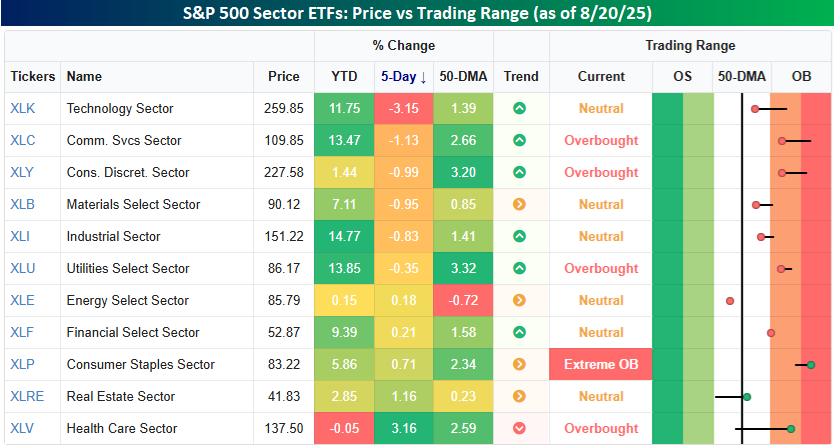

It’s been a mixed picture in terms of sector performance over the last week. Technology (XLK) has been the biggest loser, declining 3.2%, moving it out of overbought territory. Besides tech, the only other sector down more than 1% is Communication Services (XLC), while Consumer Discretionary (XLY) and Materials (XLB) are down just shy of a percent. At the other end of the spectrum, it has been defensive sectors holding up the best, just as you would expect during a market pullback. Health Care (XLV), the only sector down YTD, is up 3.2% while Real Estate (XLRE) and Consumer Staples (XLP) are the only two other sectors that have gained more than half a percent.

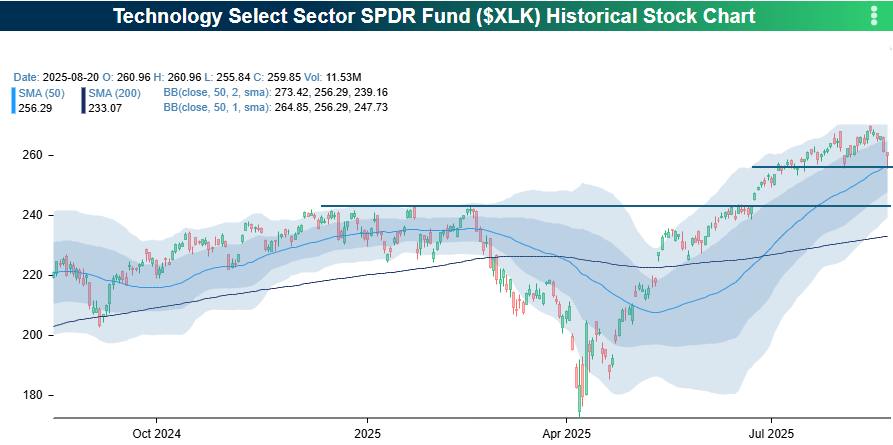

Looking at the Tech sector, at one point in yesterday’s sell-off, it tested its 50-day moving average and short-term support that coincides with other low points since the start of the second half. If these levels don’t hold, the next area to look at would be the high from earlier in the year, right before markets started to roll over. Those levels are about 7% below yesterday’s close.

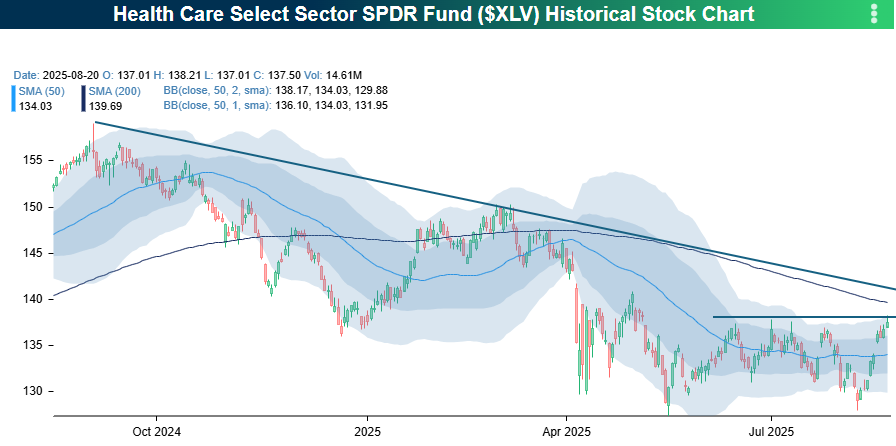

Health Care has been a completely different animal. After testing support near 52-week lows last week, the sector has now rallied back to the high end of its post-Liberation Day range. If it can break through those short-term resistance levels, the next areas to watch will be the 200-DMA, which is about 1% above yesterday’s close. After that, the downtrend line in place for a year now would be the next area to watch. If the sector can break through all these levels, we may finally be able to say that the sector is on the mend!