See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A lot of people are scared to ask questions because they don’t want people to know how dumb they are. I’ve never had that problem.” – Ken Langone

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Home Depot (HD) kicked off retailer earnings week this morning and reported weaker-than-expected EPS on slightly weaker-than-expected revenues. That’s the bad news. On a positive note, the company reaffirmed its guidance for the full year, and while most companies missing results this earnings season have been pummeled on their earnings reaction days, shares of HD are trading more than 1% higher in the pre-market. HD earnings have had little impact on futures, which are mixed on either side of the flatline. That follows what was a fractionally negative overnight session in Asia, and a fractionally positive session so far in Europe.

Here in the US this morning, besides the HD earnings report, there hasn’t been much in the way of stock-specific news. On the economic calendar, July Building Permits and Housing Starts will hit the tape at 8:30. Heading into those reports, bonds are trading slightly higher, crude oil is down 1%, gold and other precious metals are modestly high, while Bitcoin and Ether continue their recent weakness with declines of roughly 1%.

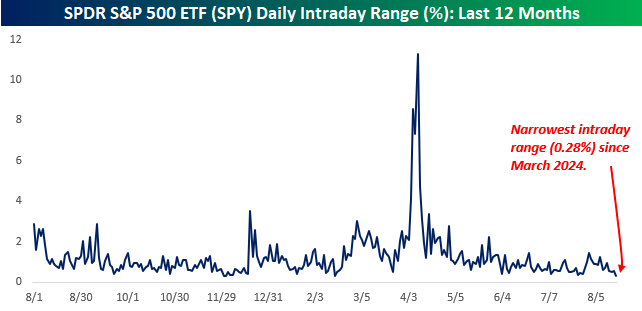

Yesterday was a tough day in the market – to stay awake. From the opening to closing bell, the SPDR S&P 500 ETF (SPY) traded in a range of 0.28% which was the narrowest intraday range since March 2024. To put yesterday’s range in perspective, the intraday range of the market on April 9th at the height of the tariff drama was more than 40 times larger.

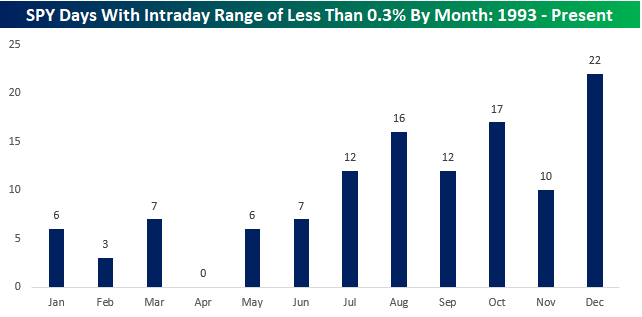

Given that we’re in August, it shouldn’t come as too much of a surprise that the market has been quiet. Since the launch of SPY back in 1993, August has seen the third-highest frequency of days when the ETF’s intraday range was narrower than 0.3%. The only two months with a higher frequency were October (17) and December (22). December makes sense given the holidays, but the fact that October has had the second-highest frequency of days with an intraday range of less than 0.3% was surprising. Digging a little deeper, we found that more than half of them (9) occurred in October 2017. That could have been the most docile month of trading in SPY’s history!

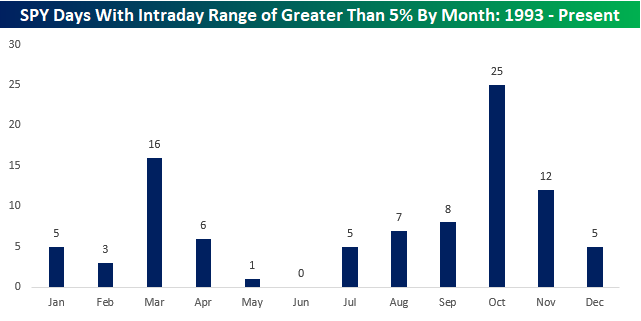

On the flip side, just for fun, we also looked at which months most frequently have seen 5% intraday ranges in SPY. Unsurprisingly, October has been the clear leader with 25, followed by March with 16. Here again, the high frequency of occurrences in March is primarily due to 2020, when there were 12, and the only four other occurrences were in 2009, around the lows of the Financial Crisis.