See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The greatest danger occurs at the moment of victory” – Napoleon Bonaparte

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

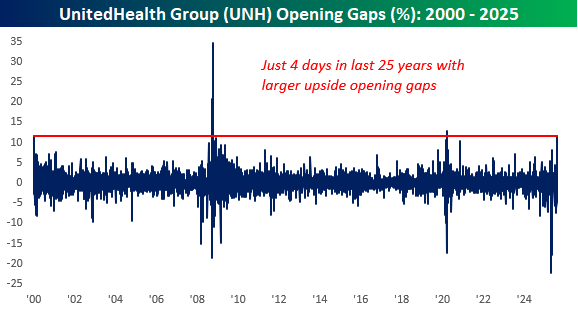

It may be a summer Friday, but there’s plenty of economic data to deal with this morning as Retail Sales and Import Prices were released at 8:30. At 9:15, we’ll get updates on Industrial Production and Capacity Utilization, and then at 10, Business Inventories and preliminary Michigan Sentiment will hit the tape. Heading into all the data, futures were mixed. Dow futures are sharply higher, but that’s all due to an 11% rally in UnitedHealth (UNH) following news that Berkshire Hathaway (BRK/b) has acquired a $5 bln stake in the company. Based on its current price, UNH is on pace to have its fifth-largest upside opening gap in the last 25 years.

It’s worth noting, though, that with the stock trading at $303 in the pre-market, it’s still trading more than 20% below its average closing price in Q2. We have no way of knowing Buffett’s cost basis on the position, but the odds are that Buffett is still underwater or barely positive on the position.

In Asia overnight, the Nikkei reversed Thursday’s losses following a better-than-expected GDP report and finished the day at another record with gains of over 1.5%. Chinese stocks were also higher, but economic data for the world’s second-largest economy missed forecasts as Retail Sales and Industrial output both came in weaker than expected.

European equities are higher across the board with modest gains as the STOXX 600 is up 0.20, led by France and Italy.

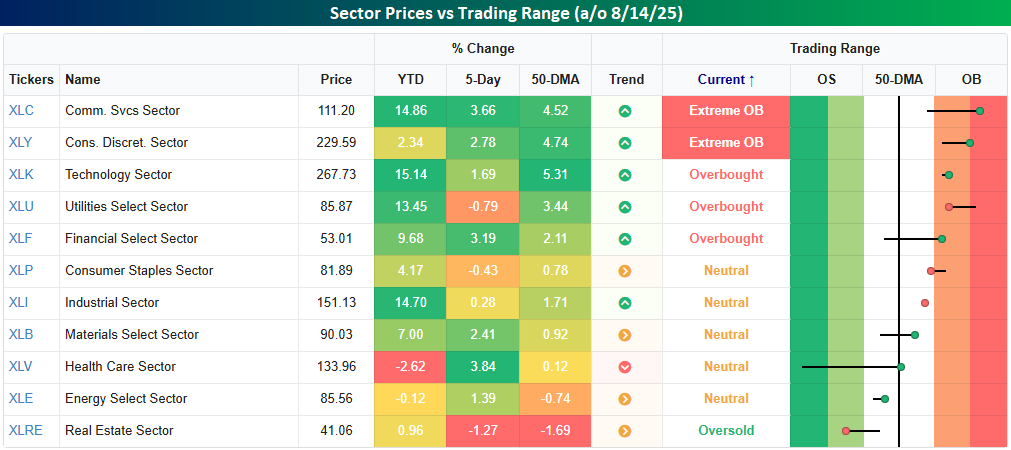

Looking through the various sectors and where they stand relative to their short-term trading ranges, we noted an interesting collection of sectors trading at overbought levels. Topping the list were Communication Services and Consumer Discretionary, which closed yesterday at ‘extreme’ overbought levels (2+ standard deviations above 50-DMA). Behind these two sectors, Technology, Utilities, and Financials all finished the day yesterday at overbought levels (1+ standard deviation above 50-DMA). It’s perfectly normal to see most of these sectors trading at overbought levels at a time when the market is in rally mode. The one exception is Utilities. Given its more defensive characteristics, Utilities tend to lag when the market is hitting all-time highs.

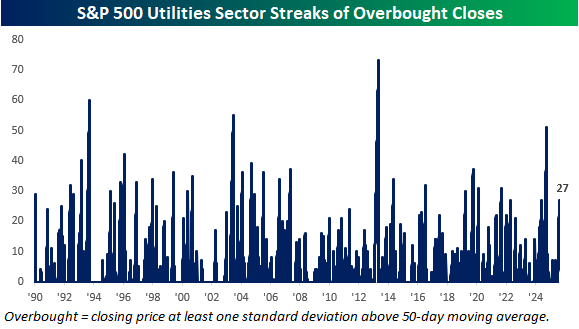

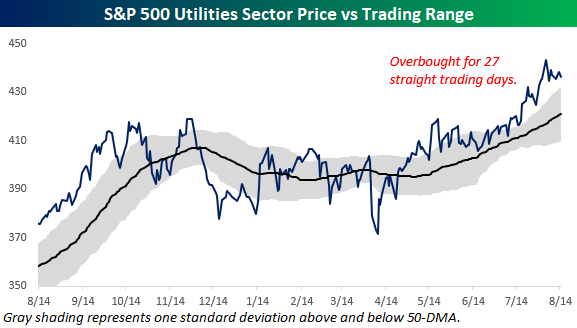

Utilities has been doing anything but lagging the broader market these days. As noted in last night’s Sector Snapshots report, the sector closed at overbought levels for the 27th day in a row yesterday.

At 27 days, the current streak of overbought closes for the Utilities sector is the longest since last October. As the chart below illustrates, though, this current streak is hardly extreme. The streak last October ended at 51 trading days, and there have been many other longer streaks in recent years.