See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“History is a sequence of random events and unpredictable choices, which is why the future is so difficult to foresee.” – Neil Armstrong

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There wasn’t much in the way of data to speak of at this time yesterday, but the pace of earnings has been strong since last night’s close, and futures are modestly higher ahead of the open with the S&P 500 indicated to open 0.26% higher while the Nasdaq is up 0.40%. The big earnings headliner overnight was Palantir (PLTR), which reported an earnings Triple Play and is trading up nearly 7%. Older economy stocks, however, aren’t faring as well this morning, with Caterpillar (CAT) trading down 3.6%.

The only reports on today’s economic calendar are the Trade Balance at 8:30 a.m. and the ISM Services report at 10:00 a.m. Economists expect the reading to bounce to 51.5, up from 50.8 last month.

Overnight and this morning, global equities have been broadly higher. In Asia, India’s Sensex was the only major index to finish the session lower, while China was up 1% and the Nikkei added 0.6%. Besides follow-through from Monday’s US session, stocks in the region were boosted by positive PMI readings. In Europe, the STOXX 600 was up 0.5% following a mixed batch of PMI readings for the Services sector.

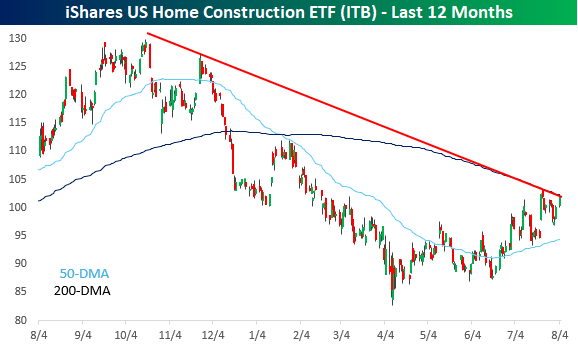

While the equity market reversed much of Friday’s losses on Monday, Treasury yields saw little to no reversal. Take the 10-year yield, for example. After closing at 4.37% last Thursday, the yield plunged to 4.22% on Friday after the jobs report, but on Monday, yields fell even further and finished the day below 4.2%. This morning, yields are slightly higher, but only at the level they closed out last week. At these levels, yields are right near their lowest levels since Liberation Day in early April. The trillion-dollar question for investors now is whether the drop in yields is due to the market pricing in lower inflation or lower economic growth, as they have very different implications for the direction of the equity market.

One sector that should benefit from lower yields is homebuilders. The iShares Home Construction ETF (ITB) has rallied 23% off its April lows, but it is still more than 20% off its 52-week high from last summer, so if the drop in yields was due to lower inflation, the group would presumably have plenty of room for more upside. From a technical perspective, ITB finds itself at an important juncture just below its downtrend that has been in place since last summer’s high, as well as the downward-sloping 200-day moving average. A rally in January failed at that level, but the ETF is heading into the latest test with a more established uptrend in place.