See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Any fool can make something complicated. It takes a genius to make it simple.” – Woody Guthrie

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The President’s letter-writing campaign to global trading partners continued over the weekend with notifications sent to Mexico and the EU informing them that if no trade deals are reached before August 1st, they will face tariffs of 30% on all products sold into the US. When these types of rates were first announced in April, they nearly pushed the S&P 500 into a bear market. This morning, S&P 500 futures are down just fractionally and within a couple of percentage points of all-time highs. Investors are betting that tariff rates at these levels will never go into effect, and while 30% is the unlikely long-term figure, the lack of concern today is the opposite of the panic three months ago.

Along with the weakness in US futures, European stocks are also trading down fractionally. Germany, the largest exporter in the EU, is leading the way down with a decline of 1%. Overnight, in Asia, most markets were also fractionally lower, so it’s not just US investors who are yawning at the latest batch of letters from the President.

The most action this morning is once again in the crypto pace as Bitcoin continues its march to record highs and traded well over $120K. Ether has also been getting in on the act with a 2% rally this morning and back above $3K.

Besides tariffs, the upcoming week will be an important one on the economic front with the release of June CPI (Tuesday) and PPI (Wednesday). Economists have been waiting (and waiting) for tariffs to push inflation readings higher, but those concerns have yet to manifest themselves in the official numbers.

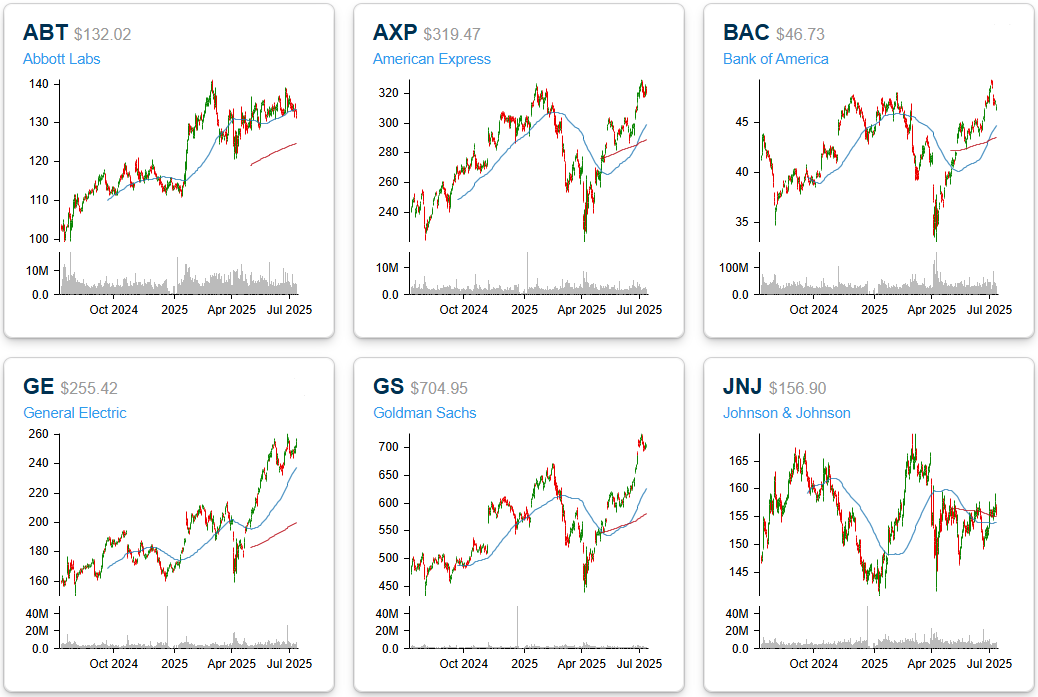

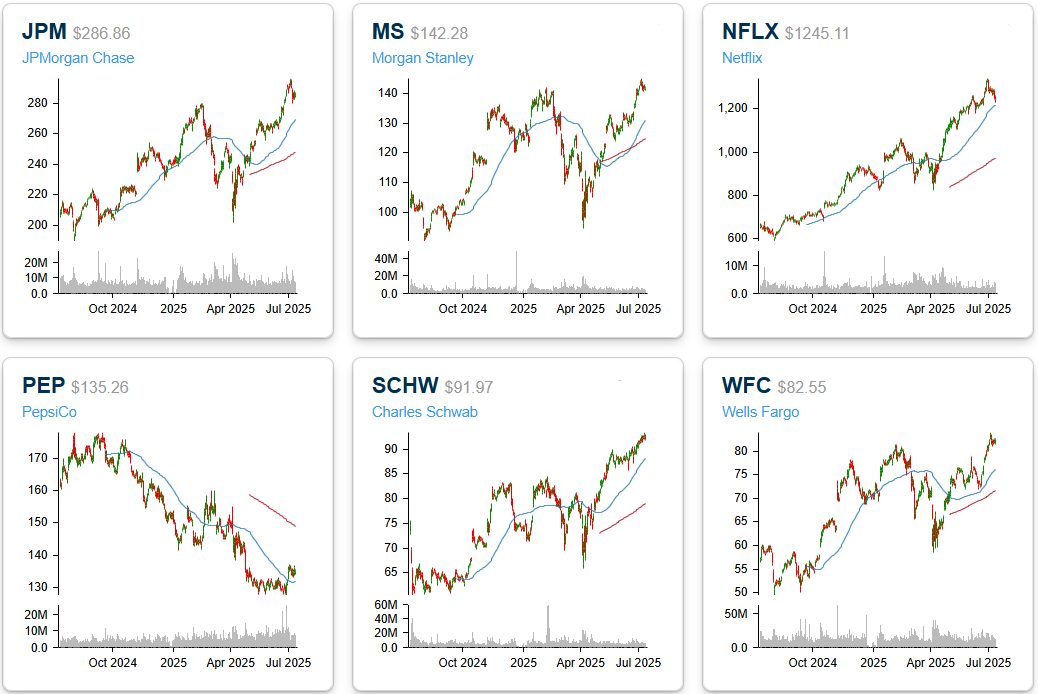

Tariffs are driving headlines this morning, but earnings (which will ultimately at least be partly impacted by tariffs) will start grabbing headlines beginning this week as Q2 earnings season gets underway. The major banks and brokers will be the main area of focus for the week. Still, other notable non-financial sector stocks reporting include Johnson & Johnson (JNJ) on Wednesday, and then Netflix (NFLX), General Electric (GE), Abbot Labs (ABT), and Pepsi (PEP) on Thursday.

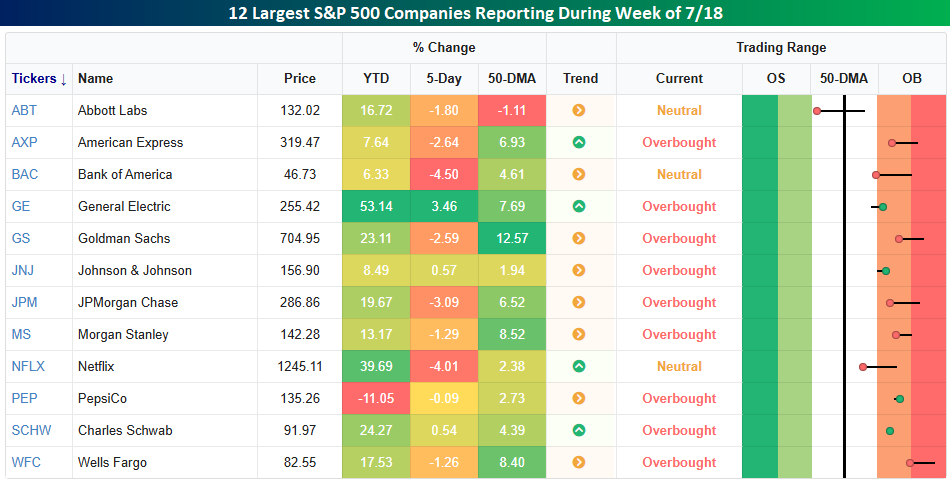

The S&P 500 finished last week down by 0.3%, but of the 12 largest S&P 500 companies scheduled to report, eight of them underperformed the S&P 500 last week, indicating that some investors took profits after the strong runs they had over the last three months. That can be considered a modest positive as it suggests investors aren’t being overly complacent ahead of their respective reports. They have still mostly performed well over the last three months, though. As shown in the snapshot below, nine of the twelve stocks shown finished the week at overbought levels (1+ standard deviation above their 50-DMA), and only ABT is below its 50-DMA.

Below we show one-year charts of each of the twelve largest stocks scheduled to report earnings this week. Except for JNJ and PEP, all twelve are either at or not far from 52-week highs. Goldman Sachs (GS) is one name that has seemingly gone parabolic over the last three months. Despite trading down 2.6% last week, the stock is still up over 40% since its last earnings report in April, which ranks as the three strongest performances between earnings reports for the stock on record.