Few Shorts Feeling the Pain From FANG Stocks

If you follow the market even remotely, you know that Q1 was a period where the FANG stocks of Facebook, Amazon, Netflix, and Google Alphabet came back into favor. Just in the last several trading days, shares of Amazon (AMZN) have broken out to new highs on the back of a six-trading day winning streak where the company has added nearly the equivalent of an entire Target (TGT) to its market cap! Looking at the performance of AMZN and the rest of the FANG stocks in recent months, one thing that sticks out at first glance is how few of the short sellers have been hurt along the ride. In many cases, when you see stocks rally in the way that these four stocks have run, traders may start to bet against the companies on the premise that they have gotten ahead of themselves. For the four FANG stocks, though, it seems as though short-sellers have been laying out the red carpet.

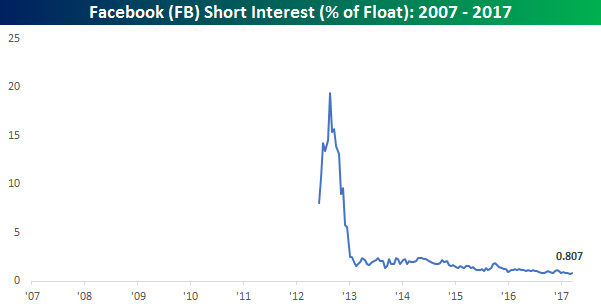

As exhibit A, take a look at Facebook (FB). As of the most recent data, short interest as a percentage of float in FB is under 1% of the free-floating shares, or 0.807%. Since the company came public, there have only been two other times where short interest as a percentage of float for the company was lower and they were both this year. For some perspective, short interest as a % of float for the company was over 15% after it first came public and over 2% three years ago.

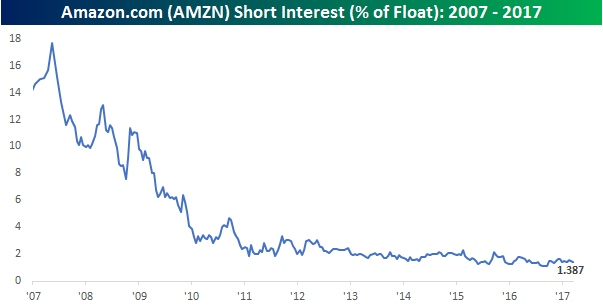

For AMZN, short interest is almost as scarce. At a level of 1.387%, short interest in AMZN is also near historically low levels.

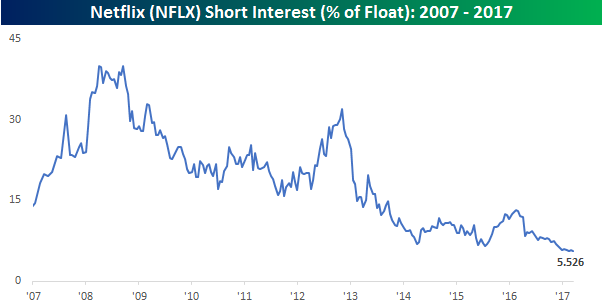

Netflix (NFLX) is a similar story. While its short interest as a % of float is the highest of the four FANG stocks at 5.526%, it is the lowest level that NFLX has ever seen. As recently as late 2012, its short interest as a % of float was over 30%, and just over a year ago, it was more than double its current levels.

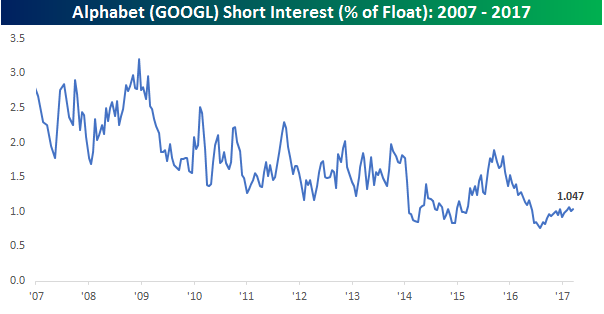

Finally, for Alphabet (GOOGL) its short interest as a percentage of float has actually been increasing in the last several months, but at a level of just over 1% is still extremely low.

At first glance, it appears as though there is very little pessimism in the market towards these stock, and from a contrarian perspective, when everyone is leaning one way, the market usually doesn’t follow suit. That’s certainly a valid argument, but there is one important thing to keep in mind. All four of these companies are mega-cap stocks, and because they are so large, mega-cap stocks typically have low levels of short interest. For example, non-FANG stocks with similar market caps such as Exxon Mobil (XOM), Microsoft (MSFT), JP Morgan (JPM) and Johnson & Johnson (JNJ) also all have less than 1% of their float sold short. In fact, the average short interest as a % of float for the ten largest non-FANG stocks in the S&P 500 is just 0.93%. So, yes, average short interest levels of the FANG stocks are at or near multi-year lows, but it is just as much, if not more a function of their extraordinarily large market caps than it is anything else. As the market caps of these companies have grown, the amount of capital on the short side hasn’t grown proportionately with them.