ETF Trends: International – 4/11/17

WTI has delivered a major rally over the last two weeks, despite a modest decline today. Energy has benefited while the Philippines and Turkey have paced global equity returns over the past week. Retail has also bounced along with bond prices and REITs. Despite the oil rally, Russia has been the worst performing ETF over the past week. South Korea and Brazil have both declined along with steel, base metals, banks, and semiconductors.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Bespoke CNBC Appearance (4/10/17)

Bespoke co-founder Paul Hickey appeared on CNBC’s Power Lunch yesterday to discuss markets ahead of earnings season. To view the segment, please click on the image below.

The Closer — Retail Valuation, LMCI Update — 4/10/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at valuation in the retail sector and update our tracking of the Fed’s unofficial labor market conditions index.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

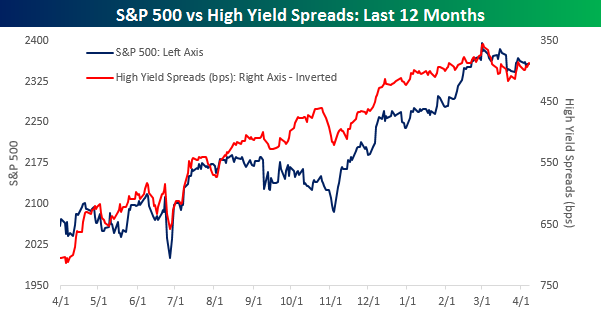

High Yield Spreads Tracking Equity Prices

Learn more about Bespoke’s research and wealth management services.

Whenever we are looking for positive or negative divergences in the equity market, one area we look to is the high yield credit market. Here, we look to see how spreads on high yield debt relative to treasuries are trending over time. If you are unfamiliar with the term, when we use the term spreads we are simply referring to the difference in yield between a high yield debt security and the yield of a US treasury with a similar maturity. Generally speaking, rising spreads in the high yield market indicate an increase in risk aversion on the part of investors as the higher spread indicates that investors are requiring higher compensation in exchange for taking on the credit risk. Conversely, when spreads are narrowing it indicates that investors are willing to take less in the way of compensation for the particular credit risk.

In the chart below, we have plotted the S&P 500 (blue line) versus high yield spreads (red line) based on the Merrill Lynch High Yield Master II Index. However, since spreads tend to move in the opposite direction as prices, we have plotted them on an inverse basis in order to make it easier to compare the two. Looking at the chart, high yield spreads and the equity market have generally tracked each other pretty closely over time. The only period of divergence was a positive one in the summer, where the S&P 500 was drifting lower while spreads continued to narrow. Ultimately, that divergence was a good reason to stay positive even during the uncertainty regarding the election.

Fast-forwarding to the present, high yield spreads have been tracking the S&P 500 pretty closely over the last several weeks. In fact, the S&P 500 saw its most recent peak just as spreads in the high yield market reached their narrowest levels, and since their respective extremes, the S&P 500 has been drifting lower as spreads have been listlessly moving higher. If you’re a bull, in an ideal world you would prefer to see spreads remaining near their narrowest levels or making new lows during this period of consolidation for the S&P 500, but at this point judging by the movement in the high yield market, there is nothing to suggest that the last six weeks of trading have been anything more than a pause.