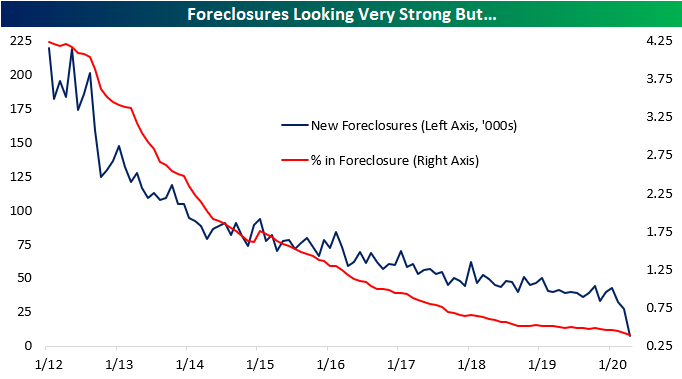

Foreclosures at Record Lows But…

In May 5th’s Closer earlier this month, we noted how monthly Black Knight mortgage data for March with some caveats was holding up despite the economic impacts of the pandemic. Yesterday, Black Knight released their first look at April’s data. The release had some positives but overall gave a fairly bleak outlook. Starting with the good news, both new foreclosures (7,400) and the foreclosure rate (0.4%) fell to record lows in April. But the good news essentially stops there as that was largely a result of moratoriums on foreclosure activity rather than an actual improvement in borrower payments.

Delinquencies, on the other hand, were sharply on the rise with 6.45% of all loans now delinquent. That nearly doubled March’s rate of 3.39% for the largest month over month increase on record which was also nearly 3x the size of the prior record from 2008 as reported by Black Knight (note: that 2008 occurrence is not shown in chart below as our data only dates to 2012). While not the case yet, those delinquencies may filter through to a rise in foreclosures down the road depending on how fast households can recover from the COVID shock to incomes.

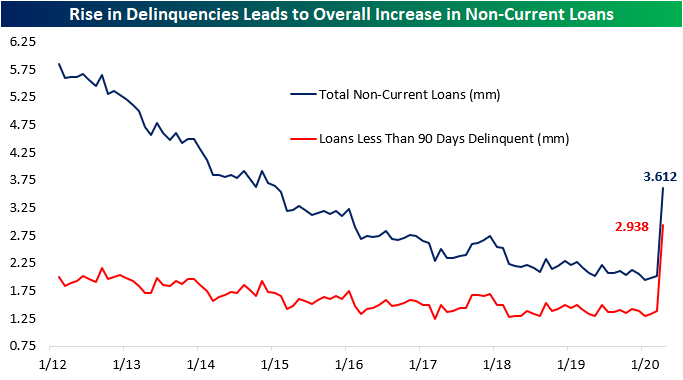

Despite the lower foreclosures at the moment, the uptick in delinquencies leaves the sum of non-current loans at 3.612 million which is the highest since January of 2015. This sort of data is why headline indicators of housing market health like existing home sales should be treated cautiously; they’re in effect missing the lagged effects on incomes that delinquency stats capture. Start a two-week free trial to Bespoke Premium to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – 5/22/20 – Quiet Finish

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

It wasn’t looking like a positive end to the week for equities, but futures have bounced in the last hour or so, and are now pointing to a flat to slightly positive open. The data calendar is quiet this morning, and barring any major headlines, trading is likely to slow down as the day progresses heading into the holiday weekend.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, news in global markets, global and national trends related to the COVID-19 outbreak, and much more.

New laws from China related to curtailing civil liberties in Hong Kong have raised concerns over a new round of protests in the region, and the result was a steep sell-off in Hong Kong stocks overnight. The benchmark Hang Seng (HSI) fell over 5.5% for its weakest one-day decline since 7/8/15. Since 2000, last night’s decline was the 24th time since 2000 that the Hang Seng (HSI) dropped more than 5% in a single session. Following those 23 prior occurrences, the HSI saw an average gain of 1.2% (median: 1.7%) the following day with positive returns 70% of the time. While the HSI tended to bounce back a bit the following day, the average change over the following month wasn’t nearly as strong with an average and median decline of -0.2% and positive returns less than half of the time (48%).

For the here and now, last night’s decline in the HSI was a bit discouraging as the index broke down after several failed attempts to break above short-term resistance.

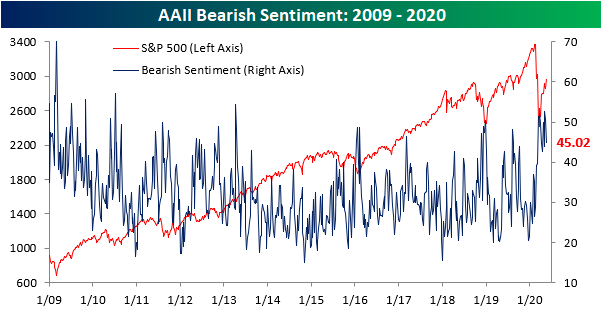

Bears Slow to Back Off

With the S&P 500 up around 4% since last Thursday’s close, bullish sentiment has unsurprisingly picked up with the percentage of investors reporting as bullish in AAII’s survey rising to 29% this week off of the recent low of 23.31% last week. At that level, bullish sentiment still remains low below levels seen as recently as the last week of April when it was at 30.6%.

The bulk of investors remain bearish. A little over 45% reported as such this week which was an improvement from readings of over 50% over the past two weeks. Similar to bullish sentiment, that leaves bearish sentiment at its lowest level since the last week of April.

While improved, bearish sentiment remains elevated relative to its historical readings as it has been for some time now. In fact, it has been above its historical average of 30.5% for 13 consecutive weeks now. That is tied with another 13-week long streak that lasted from the end of 2018 through the first weeks of 2019 for the longest stretch of above-average bearish readings since a 15-week long run that ended in August of 2012. Granted, that is not nearly as long of a time of high bearish readings as was seen in the years of the Financial Crisis. Back then bearish sentiment came in above average for 83 straight weeks. But as shown in the second chart below, bearish sentiment has not only been just above average. It has been so by at least one standard deviation for 11 straight weeks. That is now the fourth-longest steak on record and the longest since 2008’s 14-week run.

Neutral sentiment has been pretty stable with around a quarter of respondents reporting as such over the past several weeks. After recovering from its multiyear low of 14.5% in March, neutral sentiment has remained within two percentage points of 25% for each of the past five weeks. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: A Tale Of Two Issuances

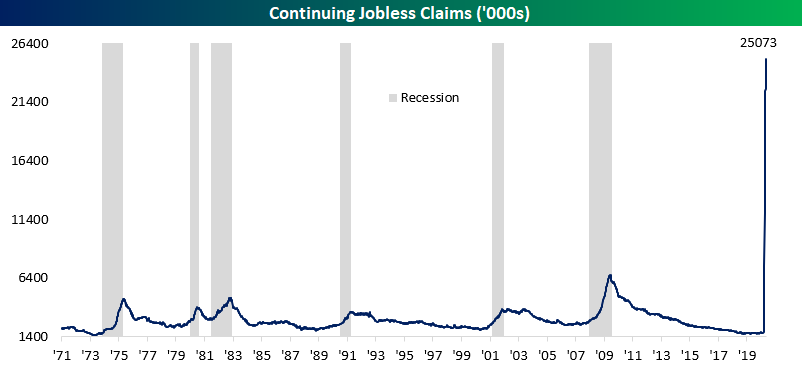

Claims Continue to Fall, Continuing Claims Continue to Rise

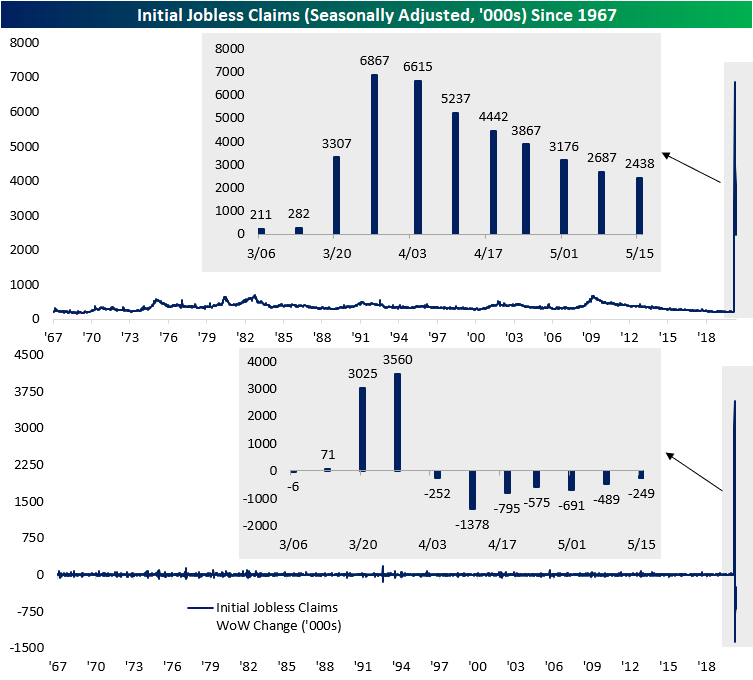

For the seventh week in a row, jobless claims have been falling coming in at 2.438 million which was above forecasts of 2.4 million. This week’s 2.438 million number is the lowest claims data point since the first spike in March. That is certainly a positive as those declines are a sign of improvement, but claims also continue to print at much higher levels than anything observed prior to COVID-19 as the running total since the first print over one million in March now stands at 38.6 million. That is roughly 11.8% of the US population or 23.5% of the labor force.

As previously mentioned, this was the seventh consecutive week in which jobless claims declined week over week. As shown in the chart below that is an unprecedented streak. In the data going back to the late 1960s, there have only been two other stretches of seven weeks of declines: one ending in October of 1980 and another ending in November of 2013. Given jobless claims are at such extremely high levels and have very far to fall until they return to normal, this streak certainly could keep growing.

As for the non-seasonally adjusted data, this was only the sixth consecutive week with a decline, but this week’s 2.174 million number, as with the seasonally adjusted number, is also the lowest print since the first of the extreme readings in March.

The four week moving average has also continued to decline consistently falling for a fourth straight week down to 3.042 million. While an improvement, this week’s decline of 501K was the smallest week over week decline since the four week moving average began to turn around four weeks ago.

Again while initial jobless claims have been improving in recent weeks, a massive number of people in the US remain unemployed. Although lagged one week to initial jobless claims, continuing jobless claims came in at a record 25.073 million this week. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – 5/21/20 – Semis Strong

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

In a busy day for economic data, Philly Fed, Initial Jobless Claims, and Continuing Claims have all been released so far and all three missed expectations. Still on the calendar, we have preliminary Markit PMI data, Leading Indicators, and Existing Home Sales. Futures were moderately lower early on, but have actually started to pick up steam in the aftermath of the data.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, the latest news in global markets, preliminary PMI data, the latest global and national trends related to the COVID-19 outbreak, and much more.

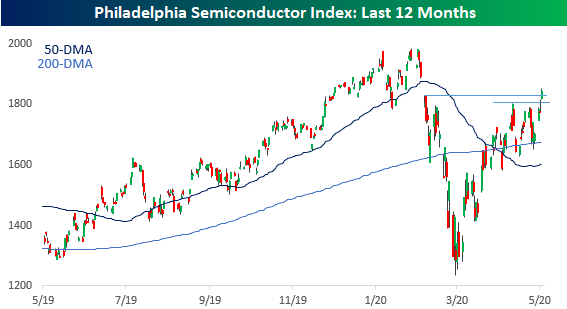

Yesterday was a strong day for semis as the group broke above short-term resistance and also into the gap from its decline on 2/24 when it gapped down below its 200-DMA. Semis the ‘Transports of the 21st Century and strength from this sector is an encouraging trend for the broader market.

Fixed Income Weekly – 5/20/20

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we take a look at high yield sectors that have taken big hits from COVID.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Bond ETFs Break Out

Over the past few days, there have been some notable breakouts for some of the largest fixed-income ETFs. The High Yield Corporate Bond ETF (HYG) currently is only in the middle of its range that has been in place since early April. In the past couple of weeks, HYG broke above the downtrend line off its pre-COVID highs, but. In the past few sessions, it has successfully retested that downtrend line before surging higher this week.

As for investment-grade corporate bonds (LQD), after reaching a new high on March 6th, the ETF plummeted over 21% through March 19th but quickly recovered much of those losses and was within two percentage points of that prior high as soon as April 9th. It never quite reached those levels, though, and had been in a downtrend since then. After successfully testing support at its 200-DMA last Monday, a day before the Fed’s corporate bond ETF buying program began, LQD has consistently been on the rise and is breaking above that downtrend this week.

Action by the Fed definitely played a role in alleviating issues in the corporate bond space, but for municipal bonds the aid has been slower to come. The Fed’s announced facility for munis is not projected to be fully up and running until the end of the month. Despite that, the Muni Bond ETF (MUB) is also eyeing a breakout above its mid-April high.

While all of these ETFs are breaking out, their performance since March 23rd when the equity market found a bottom and the Fed announced corporate credit facilities has varied a bit. HYG and LQD managed to rise 16.86% and 12.87%, respectively, as of yesterday’s close. Meanwhile, without the same central bank aid up until more recently, MUB has underperformed only rising 9.2% as shown below.

Credit spreads echo the outperformance of corporates. Again since 3/23, corporate credit has been rallying versus UST, but the opposite holds true when it comes to munis as spreads have been consistently on the rise in that same time frame. Start a two-week free trial to Bespoke Institutional to access our Fixed Income Weekly and much more.

Lowe’s (LOW) Close to New Highs

Home improvement retailer Lowe’s (LOW) reported quarterly earnings this morning and blew away numbers. EPS came in at $1.77 versus a consensus estimate of $1.32, while revenues came in at $19.675 billion versus a consensus estimate of $18.28 billion. In pre-market trading, LOW is up 5.7%, and shares are within $3 of all-time highs that were made on February 20th (one day after the S&P 500 peaked).

The price chart of Lowe’s is one to behold, and it really makes you wonder how “the market” could have gotten it so wrong. Prior to the stock’s collapse at the height of the COVID scare, it had been in a strong, long-term uptrend. LOW last reported earnings on February 26th, just a few trading days after its last all-time high was made. In between today’s earnings report and its last earnings report three months ago, the stock experienced a 48% decline — essentially cut in half — followed by a 90% rally. During its 48% rout in less than a month, investors certainly weren’t thinking that LOW would turn out to be a huge winner from the COVID lockdowns. But just as quickly as it declined, the stock surged back as more investors realized that lockdowns and stay at home orders meant consumers would use the period to do all the things around the house that had been put off over the years. It also helped that most residential construction projects were not put on hold throughout the lockdowns, and that home improvement was one of the few “lucky” areas in retail that was deemed “essential.” Start a two-week free trial to one of Bespoke’s premium research memberships for our best market anaysis.