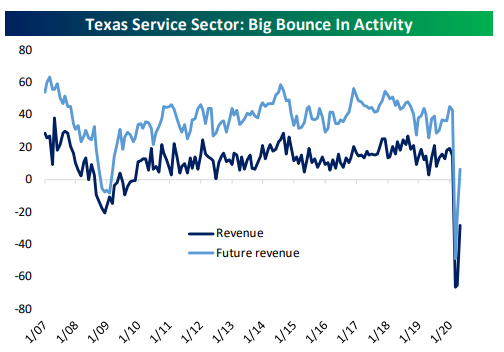

Texas Activity Starting To Recover

Yesterday the Dallas Fed released monthly activity surveys for the services and retail sectors in May. These surveys are similar to PMIs, with readings above zero indicating more respondents seeing improvement than those seeing declines, and vice-versa. Looking at revenue first, Services businesses reported much less widespread revenue declines than in April. As a reminder, though, a reading below zero still indicates revenue declines, so the May reading still indicates widespread drops in Services spending; that said, the outlook has bounced back into positive territory, which is a great sign.

Retail businesses specifically have seen an even bigger bounce in revenues that brings that state’s retail sector to almost zero revenue declines in May. Retail businesses report an even more dramatic reading for future revenue expectations, with the series in totally normal territory at this point.

Finally, we note that while revenues look to be firming up, employment is still dropping and there isn’t a big surge in re-hiring yet for services businesses. The company outlook category, despite having half of its drop reversed, is still about where it was at the lows of the last recession. Start a two-week free trial to Bespoke Institutional to access our full research platform and our unique investor tools.

Chart of the Day: Continuing Claims Peaks Mean It’s Not Too Late

Continuing Claims Improve With A Caveat

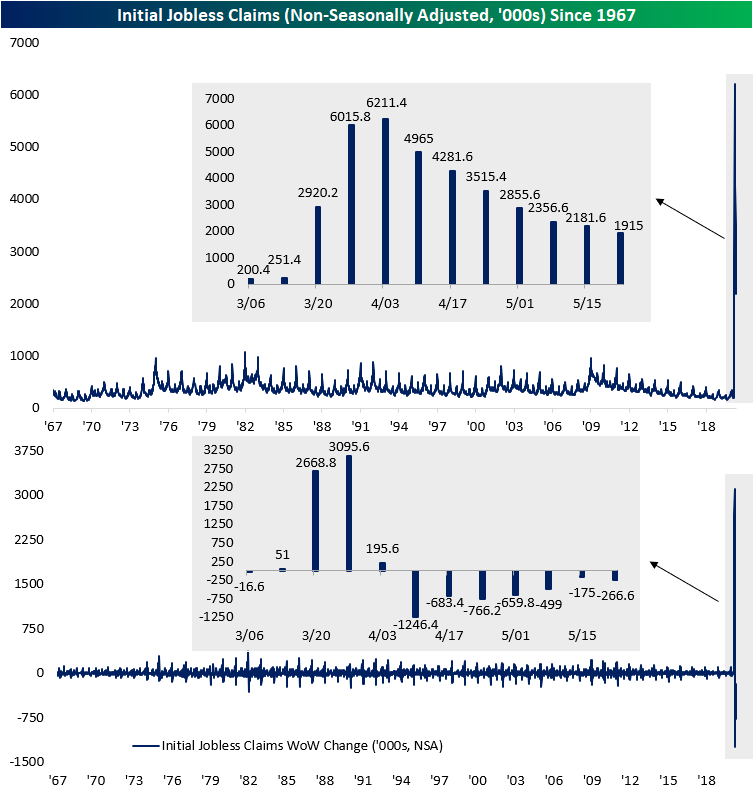

There has been a massive slate of economic data today including one of the most widely watched indicators of late: initial jobless claims. Claims fell again this week down to 2.123 million compared to a downward revised 2.446 million last week. Although lower, this week’s number was slightly above estimates of a 2.1 million print.

As we noted last week, although it doesn’t take from the fact that over 40 million jobless claims have been filed since the week of March 20th and claims continue to come in at higher levels than anything observed prior to COVID-19, they have been improving over the past couple of months. This week marked an eighth consecutive week with initial jobless claims declining sequentially. As shown in the chart below, that streak is now the longest ever, surpassing two seven week long streaks from October of 1980 and November of 2013.

As for the non seasonally adjusted data, it has only fallen for seven consecutive weeks now with the decline to 1.915 million this week. This week also marked the first sub-2 million NSA claims print since they first exploded higher at the end of March.

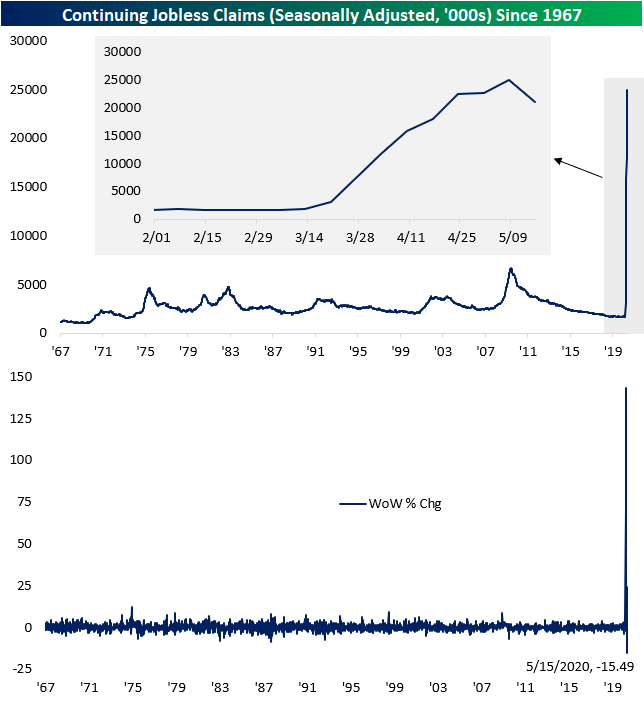

Albeit the labor market picture is still weak, initial jobless claims grinding lower in recent weeks is a positive. With states beginning to reopen, continuing claims are also beginning to fall. Seasonally adjusted continuing jobless claims fell to 21.052 million this week (NSA=19.052 million from 22.794 million last week). That is a massive 3.86 million or 15.49% drop from last week. That is the largest one week decline ever recorded (as was the NSA WoW decline of 16.42%) but that comes with a bit of a caveat.

While continuing claims dropped, the improvement is potentially less dramatic than the headline numbers imply. For instance, the bulk of this week’s decline in the US total is thanks to extremely large and yet to be explained 40.46% sequential decline in California and an even larger 76.35% decline in Florida. Washington continuing claims also experienced a smaller but nonetheless significant decline of 39.69% WoW. For Washington and Florida those were the largest one week drops on record. As for California, it was the largest one week decline since a 40.72% decline two weeks ago. While those massive declines could absolutely be legitimate, the sheer degree of the move should be handled with some skepticism especially given issues with state reporting like in Connecticut and Massachusetts in recent weeks and hiccups in Florida regarding work search questions. Excluding the enormous moves of these three states, continuing claims would fortunately still be lower, but at a more modest 1.51%. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – 5/28/20 – Zero, Nada, Zilch

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

As shown on the first page of our Morning Lineup today, there has been a ton of economic data to contend with, so we won’t go over it all here. The key (and most timely) report we would highlight is jobless claims. This morning’s reading came in at 2.123 million, which was a bit higher than expectations (2.1 million) but down from last week. In no means do we want to sugarcoat this report; 2 million claims is a ridiculously high number. We can take some solace in the fact that claims are moving in the right direction, though. This week’s reading was the 8th straight w/w decline, which is the longest such streak of declines on record (going back to 1962).

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, news in global markets, global and national trends related to the COVID-19 outbreak, and much more.

In a post yesterday, we highlighted the fact that there were only four stocks in the entire S&P 500 that were more than 5% below their 50-day moving average. With so few stocks below their 50-DMA that also leaves a limited supply of candidates to be oversold (more than 1 standard deviation below their 50-DMA), and as of yesterday’s close, there were actually zero stocks in the S&P 500 that were trading at oversold levels. That is not only the first time in at least a year that there were no oversold stocks in the S&P 500, but based on a quick scan of our database going back to 2007, there has never been another time when no stocks in the S&P 500 were oversold. Conversely, the last time more than 70% of stocks in the S&P 500 were overbought (as is the case now), was back in February 2019.

“Not So Fast”

While everyone was busy writing the Nasdaq’s obituary this morning, the index responded, “Not so fast.” After falling more than 2% intraday, the Nasdaq erased all of the early declines and not only finished higher, but it actually saw a healthy gain of over 0.5%. To put today’s move in perspective, even with the volatility of the last several months, the last time we saw a similar positive reversal (down 2%+ intraday, finished up 0.5%+) was back in February 2018 (2/6 and 2/9).

Before the two occurrences in February 2008, you have to go all the way back to the Financial Crisis to find another occurrence when there were nine in the period spanning January 2008 through February 2009. The real sweet spot for these types of reversals, though, was in the late 1990s and early 200s. In the runup to the March 2000 peak, there were ten similar reversals and then another 22 from the dot-com peak through the 2002 low. As for the Nasdaq’s return going forward, unfortunately, these types of reversals aren’t indicative of much besides the fact that there was an upside reversal that day. Start a two-week free trial to Bespoke Institutional to access all of our research and interactive tools.

Another Streak Ends

After a false alarm Tuesday, the S&P 500 finally closed above its 200-day moving average (DMA) on Wednesday for the first time since 2/27.

At 57 trading days, the just-ended streak of closes below the 200-DMA was the longest streak since the 61-day stretch ending in October 2011. But while this was the longest streak below the 200-DMA for the S&P 500 in over eight years, from a longer-term perspective, it looks almost minuscule. In May 2009, the S&P 500 ended a streak of 358 trading days below its 200-DMA, and there have been a total of nine streaks that spanned more than 200 trading days. In terms of 50-trading day streaks below the 200-DMA, there have now been a total of 34.

In a just-released report, we looked at the S&P 500’s performance following similar upside breaks of the 200-DMA. For anyone interested, sign up for a monthly Bespoke Premium membership now!

Chart of the Day: Purchase Apps Setting Up Homebuilders to Surge?

The Losers

There’s been a number of different stories flowing around this morning regarding the fact that more than 90% of stocks in the S&P 500 are above their 50-day moving averages (DMA) and how that has historically been a bullish indicator for the subsequent performance of the market. Rather than focus on all of those winners, though, we wanted to look at some of the losers, namely, the S&P 500 stocks that are currently below their 50-DMA.

The table below lists the 34 S&P 500 stocks that were trading below their 50-DMAs as of this morning. Not only are there a relatively small number of stocks on the list, but seven of them are within 1% of their 50-DMAs and only four are more than 5% below. In other words, if the equity rally continues to have legs, this list could quickly shrink even more.

In looking through the names on the list, two notable trends stood out. First, although Energy, Financials, and Industrials are the worst performing sectors so far this year, Cincinnati Financial (CINF) is the only stock on the list from one of those sectors (Financials). Meanwhile, Technology, the top-performing sector in the S&P 500 so far this year, accounts for two of the names on the list (Motorola Solutions – MSI and Citrix Systems – CTXS). The sectors that account for the most names on the list are Consumer Staples (8), Utilities (8), and Health Care (7).

A second notable aspect of the names listed pertains to recent performance. In going through the charts of the names listed, you would expect to mostly see charts of bombed-out stocks that were so weak that they couldn’t even manage to rally in this environment. While that was the case for many of them, there were also a number of stocks that actually outperformed in the initial stages of the bear market, but have started to fall apart either later in the decline, or in many cases, after the market bottomed. The nine stocks shaded in the table below (charts below) all traded at 52-week highs at least two weeks after the S&P 500 peaked in late February. These are all generally names that investors thought would benefit from the pandemic and a prolonged decline. Now that markets have stabilized, though, and the economy appears to be on the mend, there’s been a rotation out of them. One example is Citirix Systems (CTXS). After hitting a 52-week high as recently as May 11th, it now finds itself on the loser list. Start a two-week free trial to Bespoke Institutional to access all of our research and interactive tools.

Bespoke’s Morning Lineup – 5/27/20 – It’s Not How You Start But How You Finish

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Concerns yesterday afternoon regarding tensions between the US and China have disappeared this morning, and US equity futures have bounced back following Tuesday’s last hour decline. Also helping sentiment this morning is a proposed 750 billion Euro recovery fund for member nations and reports that the Japanese government is also considering an additional $1.1 trillion in stimulus.

Airlines, cruises, and other groups hit especially hard from the COVID outbreak are surging this morning with the airlines ETF (JETS) up over 8% and the cruise operators all up over 10%.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, news in global markets, global and national trends related to the COVID-19 outbreak, and much more.

After taking into account this morning’s rally in equity futures, the S&P 500 is up over 3.5% month to date- a good month by just about every account. One part of the day where strength has been lacking, though, is the last hour of trading. Yesterday, was a prime example. What was a gain of well over 2% earlier in the day turned into only a little more than 1% by the closing bell as a late-day decline negated what would have been the S&P 500’s first close above its 200-DMA in over ten weeks.

We covered this issue in more detail in last week’s Bespoke Report, but yesterday’s intraday chart provides a good example. What was an impressive rally for the market, looked a lot less so by the end of the day and the S&P 500 ultimately was unable to close above its 200-DMA yesterday. Today it will have another chance. All we need is a strong finish- something that has been far from automatic this month.

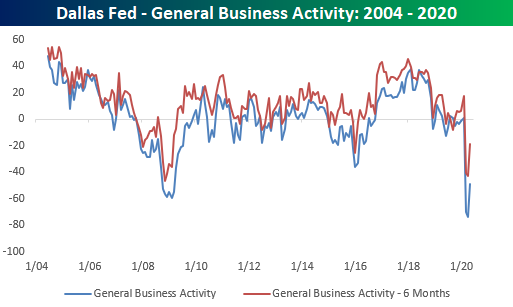

Dallas Fed Manufacturing Surges But Conditions Still Declining

This morning, the Dallas Fed updated its monthly manufacturing survey. Like other regional Federal Reserve indices of late, May saw a substantial improvement from April though the index, as well as its components, remain at extremely low levels. The 24.8 point increase from April’s -74 to May’s -49.2 was the largest one month increase on record but only leaves it in the 4th percentile of all readings. Today’s reading was also well ahead of consensus expectations for a reading of -61.0. The headline number for the six-month outlook also rose by 24 points which is in the 98th percentile of all MoM changes.

Given the improvement of the headline number, just about every component saw improvement with the exception of the index for finished good inventories which fell by 0.1 points. But that does not mean every component is showing expansionary readings. As with other regional Fed indices, conditions are still worsening just not at the same pace as in April. While it may not necessarily be a positive, only raw material prices is showing an expansionary reading (above 0). But as for six-month outlooks, the picture is a bit more optimistic.

Take a few of the components for production and demand. While current production and capacity utilization are still showing readings deep in contractionary territory, the indices for six months ahead surged to actually show expansionary readings this month. For production, that is the widest divergence between the six-month and current outlooks on record. While not at a record, the spread between the six-month and current outlook for capacity utilization is also in the 99th percentile. The same can be said for new orders and new order growth rate as both spreads are in the 95th percentile of all readings.

For production and capacity utilization, the readings this month for six-month outlook rose to pretty much within range of the past several years. In other words, Texas area manufacturers expect production to nearly return to normal in six months. The six-month outlook for new orders, though, is not as optimistic with May’s reading still much further below its range, meaning demand is not expected to ramp back up to quite the same degree as production.

As for employment, these indices seem to echo weekly jobless claims of late. Even though Texas manufacturers are still taking on fewer employees, the pace has improved from April. But there also does not appear to be much in the way of plans to expand workforces in the future. The six-month outlook for employment is still showing contraction, although hours worked are expected to rise. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.